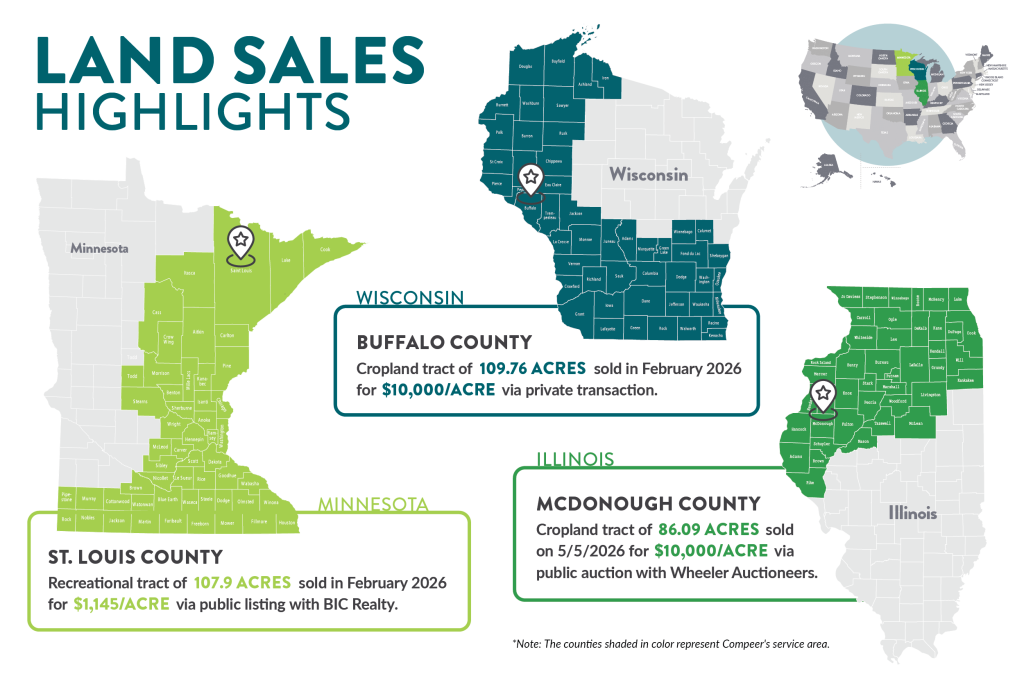

Compeer Financial’s latest Land Sales Highlights shares 3 land sales helping to tell the story of today’s ag economy from our Midwest reporting states of Illinois, Minnesota and Wisconsin. Make sure to learn more on each land sales in the links below.

Recent Notable Sales across Iowa and Wisconsin continue to demonstrate the strength of high‑quality Midwest farmland, according to reporting from American Farmland Owner.

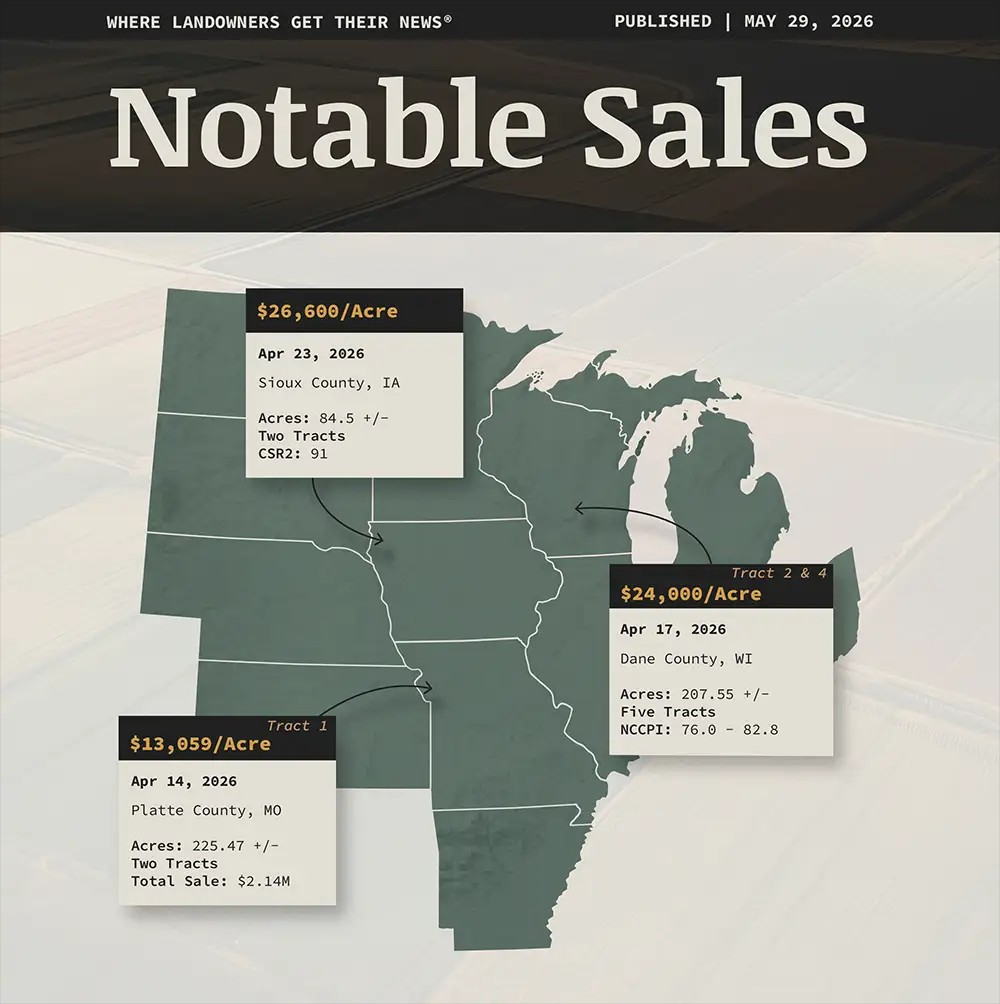

In Sioux County, Iowa, two premium cropland tracts sold for $26,600 per acre on April 2, reflecting the region’s continued demand for nearly all‑tillable farms with strong CSR2 ratings and efficient row layouts. Tract 1 included 44.5± acres with a CSR2 of 91, while Tract 2 offered 40± acres with a CSR2 of 91.8, supported by proven Galva, Primghar, and Ely soils.

In Dane County, Wisconsin, a 207.55‑acre offering brought $18,750 to $24,000 per acre across five tracts at an April 17 auction. The farm featured nearly all‑tillable acres, productive Plano, Ringwood, and Traxel silt loams, and strong proximity to Madison — all factors that contributed to competitive bidding in this tightly held region.

Michigan and it’s farmland remains one of Land Sales Bulletin’s most dynamic Midwest reporting states — a region where long‑established family farms continue to evolve, diversify, and find new markets. A recent example comes from Tekonsha, where sixth‑generation farmer Ed Shumway transformed his family’s 170‑year‑old dairy farm into a thriving international popcorn operation, shipping premium kernels to 28 countries.

Shumway’s shift from dairy to specialty crops began in the early 1990s, when he pivoted to popcorn production after years of managing a traditional dairy herd. Today, he farms roughly 700 acres, rotating popcorn and soybeans for fertility and pest management benefits. His operation extends beyond his own acres, contracting with growers in Michigan and Ohio to bring total popcorn acreage to 2,000 acres annually.

Michigan’s specialty crop strength is on full display in stories like this. From precision harvest practices — where even a cracked hull can reduce popping quality — to investments in advanced drying and cleaning systems that ensure premium kernels reach global buyers, Michigan producers continue to demonstrate the innovation and adaptability that define the state’s agricultural landscape.

Shumway Popcorn’s international reach includes markets in Jordan, Lebanon, Chile, Germany, Mexico, and Indonesia, supported by Michigan’s strong export infrastructure and state‑level resources for agricultural trade. It’s a reminder that Michigan farmland doesn’t just feed local communities — it connects to global supply chains. Farm Progress:Michigan farmer pivot to popcorn goes global

Land Sales Bulletin tracks verified farmland sales across Michigan and the broader Midwest, providing transparent, comparable data that helps landowners, operators, and ag professionals understand the trends shaping regions like this one.

A recent auction in Stoughton, Wisconsin delivered one of the most eye‑opening sales the region has seen, with a 208‑acre farm selling for $21,946 per acre—more than triple the state’s 2025 average farmland value of $6,420 per acre. Rapid‑fire bidding pushed prices upward within minutes, driven by strong demand for high‑quality cropland and limited availability in Dane County. Nearly 50 bidders participated, but a local dairy farmer ultimately secured all five tracts offered.

The sale’s momentum has already sparked new interest among landowners considering bringing properties to market, underscoring the continued strength of premium farmland in Wisconsin—Land Sales Bulletin’s home Midwest reporting state. Read more from American Farmland Owner: Wisconsin Farm Sells for Nearly $22,000 an Acre in Rapid-Fire Auction

A recent auction in west‑central Indiana showcased the continued strength of Midwest farmland—especially in regions where scale, soil quality, and location converge. The 602-acre farm, offered in seven tracts, drew 54 registered bidders and a standing‑room‑only crowd, with interest coming from seven states.

Despite the wide geographic interest, the final buyers were all local farmers or investors from west‑central Indiana, underscoring the resilience of local demand in a tightly held region. The property’s appeal was driven by three rare attributes:

Large scale — 602 acres, with 595.57 acres classified as cropland

High-quality soils — a WAPI of 172.6, unusually strong for the region

Strategic location — near major routes and within the growing “Silicon Heartland” corridor between Indianapolis and Purdue University

As one of Land Sales Bulletin’s Midwest reporting states, Indiana continues to demonstrate selective strength—particularly for Class A soils and large, contiguous tracts that rarely come to market.

Our Midwest reporting state of Wisconsin farmland values in 2026 remain remarkably steady, even after several years of rapid appreciation. Peoples Company’s recent analysis shows the market has shifted into a phase that is stable, disciplined, and highly localized.

Despite expectations of a correction due to higher interest rates and tighter margins, values across much of the state have held firm. The key stabilizers: limited supply, strong owner equity, and continued demand for high‑quality parcels.

Inventory remains the defining force. Generational ownership patterns and strong financial positions have kept many high‑quality tillable acres off the open market, reducing transaction volume across Wisconsin’s agricultural counties. When productive, well‑located parcels do list, competition is intense — especially among local operators seeking strategic expansion opportunities.

Interest rates have influenced buyer behavior but have not weakened values. Well‑capitalized buyers remain active, relying less on leverage and focusing more on operational fit and long‑term efficiency.

Quality differentiation is widening. Soil productivity, access, drainage, field configuration, and proximity to existing operations are now major determinants of value potential, with top‑tier parcels commanding clear premiums. Read more: Wisconsin Farmland Values in 2026: What’s Driving the Market

For Wisconsin landowners, 2026 remains a historically favorable environment — but outcomes increasingly depend on location, accurate pricing, and hyper‑local market knowledge. As Land Sales Bulletin continues to report verified sales across the Midwest, Wisconsin stands out as a market driven by fundamentals rather than speculation.

Farmland values in southeast Wisconsin are rising sharply, with localized increases of 25% to 35% over the past year. Some properties are now trading between $13,000 and $16,000 per acre, even as grain and milk prices remain relatively flat.

According to Compeer Financial, the primary driver behind this surge isn’t commodity strength — it’s proximity to nutrient management systems and the operational efficiencies tied to manure application logistics.

Large dairy operations in Wisconsin increasingly require nearby acreage to meet nutrient management regulations, reduce hauling distances, and control fuel and labor costs. Land located within a three‑mile radius of major livestock facilities is commanding a premium as producers compete for strategically located acres.

Competition is also expanding beyond traditional farm operators. Commercial waste processors seeking land application sites for residual materials are entering the market, adding further upward pressure in regions with limited farmland inventory.

Structural changes in Wisconsin’s dairy sector — including modernization, automation, and herd expansions from 1,500 to more than 3,000 cows — are amplifying the need for nearby cropland and reshaping local land markets.

For landowners, recent high‑profile auctions in Dodge County and areas near Madison have elevated expectations and encouraged additional listings, with private sales achieving similarly strong results. Read or listen to the full report: Farmland Near Manure Sources Fetches Premium Pricing – Compeer

While commodity prices do not fully support these valuations, location‑driven demand continues to define southeast Wisconsin’s farmland market — a trend Land Sales Bulletin will continue monitoring across our Midwest reporting region.

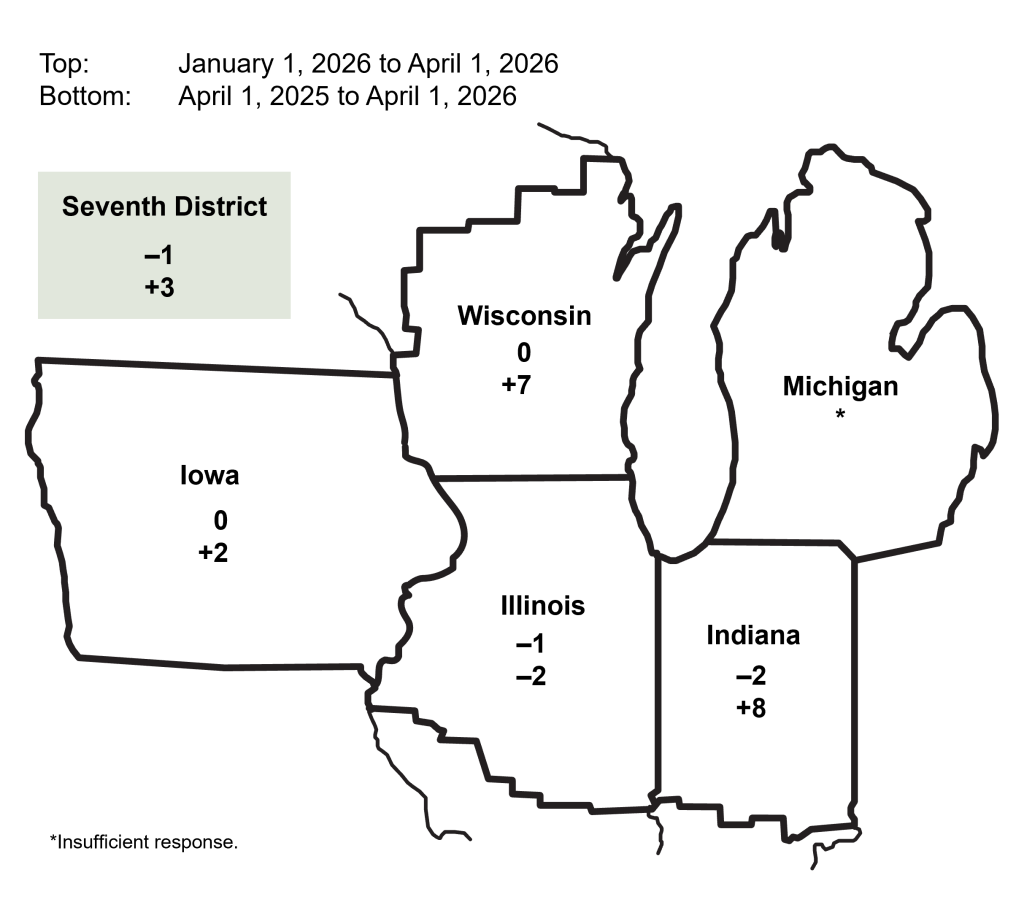

The Chicago Federal Reserve’s latest AgLetter shows that Midwest farmland values continue to demonstrate steady resilience heading into 2026. According to Seventh District data, agricultural land values were up 3% from a year earlier in the first quarter, even as “good” farmland saw a slight 1% dip from Q4 2025.

Surveyed lenders reported lower demand for farmland purchases compared with the same period last year, and the amount of farmland for sale also declined heading into early spring. Acreage sold followed the same trend, with fewer farms and fewer acres changing hands year over year.

Cash rents softened across much of the region, with the District seeing a 3% decrease in 2026—the second consecutive annual decline. State‑level shifts varied: rents were up 2% in Indiana, but down in Illinois, Iowa, and Wisconsin.

Credit conditions weakened as well. Lenders reported lower repayment rates, higher renewals and extensions, and continued strong demand for operating loans—now up for the tenth straight quarter. Nearly 17% of borrowers carried more debt into 2026 than the prior year. Read more: https://www.chicagofed.org/publications/agletter/2025-2029/may-2026

For Land Sales Bulletin’s Midwest reporting region—Illinois, Indiana, Iowa, Michigan, Minnesota, Nebraska, North Dakota, Ohio, South Dakota, and Wisconsin—these findings reinforce what our weekly finalized sales continue to show: a market adjusting to tighter credit and softer rent structures, yet still anchored by long‑term demand and the enduring strength of Midwest agriculture.

Inflation and money supply have always played an outsized role in shaping farmland markets — but their impact is especially visible across the Midwest. As the article notes, inflation erodes the purchasing power of cash, making productive assets like farmland more attractive to both farmers and investors.

Over the past decade, the U.S. money supply (M2) expanded dramatically, rising from roughly $13 trillion in 2016 to more than $22 trillion today. Much of this growth occurred during 2020–2022, when emergency fiscal spending and Federal Reserve liquidity programs injected unprecedented capital into the financial system. Read more from Farm Progress: How-does-inflation-impact-land-values

For our Midwest farmland, this matters for three reasons:

Inflation expectations drive demand for hard assets As more dollars circulate, the value of each dollar declines. The article highlights that this environment rewards asset owners and penalizes those holding cash. Farmland — with its scarcity, income potential, and long‑term stability — becomes a preferred inflation hedge.

Liquidity fuels buying power When credit is abundant, more buyers can compete for a limited supply of acres. This dynamic has supported strong appreciation across the Midwest, where local operators remain the dominant buyers.

Midwest land responds through interest rates, not speculation Unlike coastal real estate or equities, Midwest farmland values are most sensitive to interest rates, which are directly influenced by money supply trends. When M2 expands, rates tend to fall — supporting land purchases. When M2 slows, rates rise — moderating price growth.

Even as inflation cools and financial conditions tighten, the Midwest continues to show resilience. Scarcity, strong balance sheets, and productive yield help farmland hold value even when liquidity contracts.

In short: M2 sets the financial backdrop. Interest rates transmit the impact. Midwest farmland absorbs it in a steady, disciplined way.

Nebraska remains a core part of Land Sales Bulletin’s 10‑state Midwest reporting region, with recent sales activity underscoring a familiar theme across the state: strong buyer demand and limited supply. Farmland listings remain scarce, and that tight inventory continues to support values even as commodity margins shift. Landowners are cautious to sell, buyers remain active, and professionally marketed farms are moving quickly — a dynamic reflected in this month’s representative sales.

Recent Verified Sales Across Three Nebraska Counties

Saline County (Southeast) — 237.79 acres sold for $4,850/acre

219.08 tillable acres across two parcels

Mix of flat and gently rolling cropland

Working corral and pen facilities included

Lancaster County (East) — 75.16 acres sold for $8,800/acre

More than 96% tillable, with a four‑year lime program applied before 2024 planting

Geological and hydrological reports suggest irrigation potential in the northeast corner (no test drilling yet)

Pierce County (Northeast) — Two‑tract sale

Tract 1: 160 acres at $4,300/acre; 129.9 certified irrigated acres; includes 2012 Zimmatic pivot and irrigation equipment

Tract 2: 320 acres at $5,300/acre; 267.48 certified irrigated acres; includes two 2007 pivots, gearhead, and updated well components

These transactions highlight the diversity of Nebraska’s land base — from high‑quality tillable acres in the east to pivot‑irrigated tracts in the northeast — and reinforce the value of consistent, verified reporting across the Midwest. Read more from Farm Progress: Land in Demand but not much supply on the Market

Subscribers can explore full sale details, historical trends, and county‑level data through Land Sales Bulletin’s reports and digital tools.