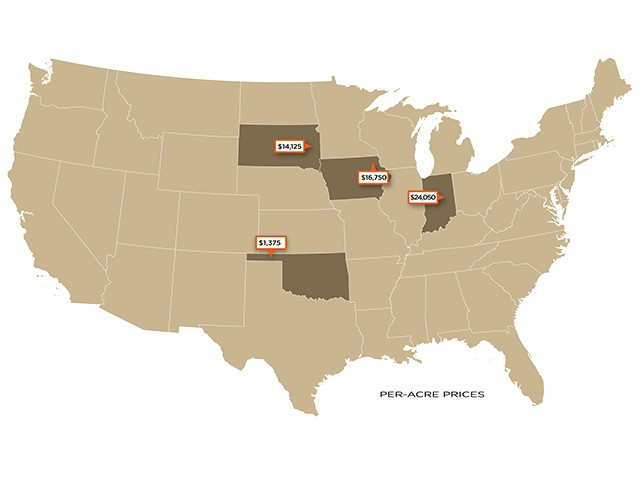

As one of Land Sales Bulletin’s Midwest reporting states, Iowa is showing early signs of a more active land market heading into late summer and fall. Here are the report highlights:

- Iowa, one of LSB’s Midwest reporting states, may see a “flush of land sales” between Aug. 1 and Sept. 30.

- Heirs who inherited land in 2024–25 may test the early‑season market before late fall and winter.

- Demand continues to outpace supply statewide, keeping conditions seller‑friendly in 2026.

- June Iowa sales showed strong pricing and competitive CSR2 ratios across multiple counties.

- A brief pause is expected during peak harvest before another strong run of sales late in the year.

Recent June sales across Iowa reinforce that seller‑friendly environment, with strong prices and competitive CSR2 ratios observed in multiple counties. Market momentum is expected to pause briefly during peak harvest before another strong run late in the year. Source: Farm Progress

Author: Doug Hensley, President of Hertz Real Estate Services

Article Link: https://www.farmprogress.com/markets-and-quotes/surge-of-iowa-farmland-sales-likely-later-this-year