Farm bill, AI expansion: 5 trends to watch in agriculture for 2024 – Agriculture Dive, January 9, 2024

2024 is said to be “ripe for changes” in the agricultural industry. Click below to read or listen to the 5 biggest trends that are said to shape the agriculture industry this year.

When Congress passed an extension of the 2018 Farm Bill as part of a broader funding package in late 2023, it bought another year to finish the job of enacting new farm bill legislation, but it didn’t make the job any easier.

The farm bill debate bogged down in 2023 over competing priorities and funding challenges, and there have already been comments and accounts of continuing the same hardened positions through 2024.

If a new farm bill is to be finished in 2024, there seemingly will need to be substantial progress and likely substantial compromise in the first half of the year before the campaign for this fall’s general election consumes all of the attention.

If not, then the farm bill seems destined for another late-year scramble after the election in a lame-duck session of Congress, or even another extension to push the issue into a new session of Congress in 2025.

When foreign investors acquire U.S. forest and farm land, they frequently are interested in the possibility of solar, wind, or renewable energy generation on their new property, said an Agriculture Department report. Companies with the words “wind,” “solar,” or “renewable” in their names hold 28 percent of the 43.4 million acres of foreign-owned or -leased agricultural land in the country.

The large increases of the past decade in foreign control of crop and pasture land “are mostly due to foreign-owned wind companies signing, as well as terminating, long-term leases on a large number of acres,” said the annual USDA report. “The actual amount of land used by a wind farm is relatively low due to the small footprint of the wind turbines and limited use of access roads. This leaves much of the parcel available for agricultural use.”

Foreign ownership of U.S. farm land has gained attention with the rise in tensions with nations such as China and Russia. During the first six months of this year, at least 15 states, some already with restrictions, enacted new laws to regulate foreign ownership of real estate, according to the Congressional Research Service. Legislation was filed in Congress to ban “adversary” nations, most commonly China, Russia, Iraq, and North Korea, from owning agricultural land or agricultural companies. Other bills would give the government more power to scrutinize purchases and block them for national security purposes.

From farmprogress.com and written by Doug Hensley, President of Hertz Real Estate Services and one of our valued API customers from the state of Iowa.

I grew up on a farm, so I know each new year always brings hopeful optimism for those in agriculture. We budget and plan based on realistic outcomes and 10 years of actual production history, but we drive and nurture to outperform those estimates. So, as I apply that same exercise to the land market, what can you expect for 2024?

We ended 2023 with a stable market, having plateaued from the incredible run-up from 2020 to 2022. In the second half of 2023, market-wide sales volume noticeably slowed in comparison to the 12 months prior, and inputs like fertilizer softened leading into the 2024 crop year. These shifts in sales volume and input prices supported land prices. However, much lower commodity prices and much higher interest rates should point the market downward.

In this 2023 tug of war, it seems recent year profits – or in other words, cash piles – were still available to power many land purchases. Therefore, strong liquidity and cash availability helped the land market remain resilient in the face of underlying pressures.

Will this continue in the new year? I expect it will, depending on the area. For the sales reported below, however, it is obvious that there is still more strength than weakness.

Despite a global economy that’s showing signs of toughness and making progress in tackling high prices, the International Monetary Fund’s October 2023 Global Economic Outlook shows bumpy roads are ahead.

Recovery from the pandemic’s ripple effects, the conflict in Ukraine and the growing divide in global trade will be like combining downed corn – slow and tough, especially for countries still developing their economies.

The world’s economic growth is expected to dip from a decent 3.5% in 2022 to just 3% in 2023, and even a bit lower to 2.9% in 2024, which is not as good as the usual 3.8% we saw from 2000 to 2019. The big economies, including ours, might see a slowdown, despite the U.S. doing a bit better than expected. However, Europe’s slower growth and issues like China’s housing market troubles are like pests in the field, affecting everyone.

Looking at the next few years, that means the global economy isn’t expected to grow as strong as we’d hope, making it harder for countries to improve living standards. And while prices might start to ease up, they’re still expected to be higher than what we’d like until at least 2025.

With all this uncertainty, is now the right time to buy farmland?

In my lifetime, farmland values have risen and fallen and risen again. Prices may continue to rise even higher than they are now, or they could retreat. The two fundamental questions we need to ask ourselves are: Is farmland a good investment? And what are the current fundamental drivers of farmland value?

Farmland has been a good investment. In the University of Illinois farmland index, we find that every $100 invested in farmland in 1979 is worth over $500 today. Research also indicates that farmland investments have produced the best returns at the lowest risk over the last 30 years.

But will farmland continue to be a good investment? Let’s look at some of the economic forces that drive farmland value today.

Following a handful of turbulent years that included a trade war, pandemic, rapid inflation, rising interest rates, a supply chain meltdown and high input costs, U.S. agriculture is hoping to find softer soil as it prepares a march through mid-decade. Here are the biggest factors to watch as 2023 comes to a close.

1. 2023 FARM INCOME

The ag economy is lukewarm, and the industry is watching to see what could trigger the financial trends of 2024.

“It’s almost impossible to repeat the level of farm income that we had in ’22,” says Jackson Tackach, chief economist with Farmer Mac. “We’re starting to really dial into what ’23 looks like, and even starting to get a good picture of 2024.”

USDA revised its net farm income forecast in August, now calling for a decline of 23% in farm income this year to $141.3 billion. That’s a drop of $41.7 billion versus last year, but it’s still the third-best year on record.

“You have to remember it’s coming down from a very large number of $183 billion in 2022,” says Michael Langemeier, associate director at the Center for Commercial Agriculture at Purdue. “Yes, it’s still a big drop, but we still have relatively strong net farm income compared with the average since 2007, which was the start of the ethanol boom.”

The challenge in 2023 has been production expenses. USDA says expenses are likely to be $458 billion, which is an almost $30 billion increase and up 7% year over year.

“Aside from fertilizer, all your other input costs are probably either stable or increasing,” says Tony Jesina, vice president of insurance at Farm Credit Services of America. “Cash rents haven’t come down yet, seed prices rarely come down, interest rates are up and family living expenses are probably not going to come down given what we’re seeing for inflation.”

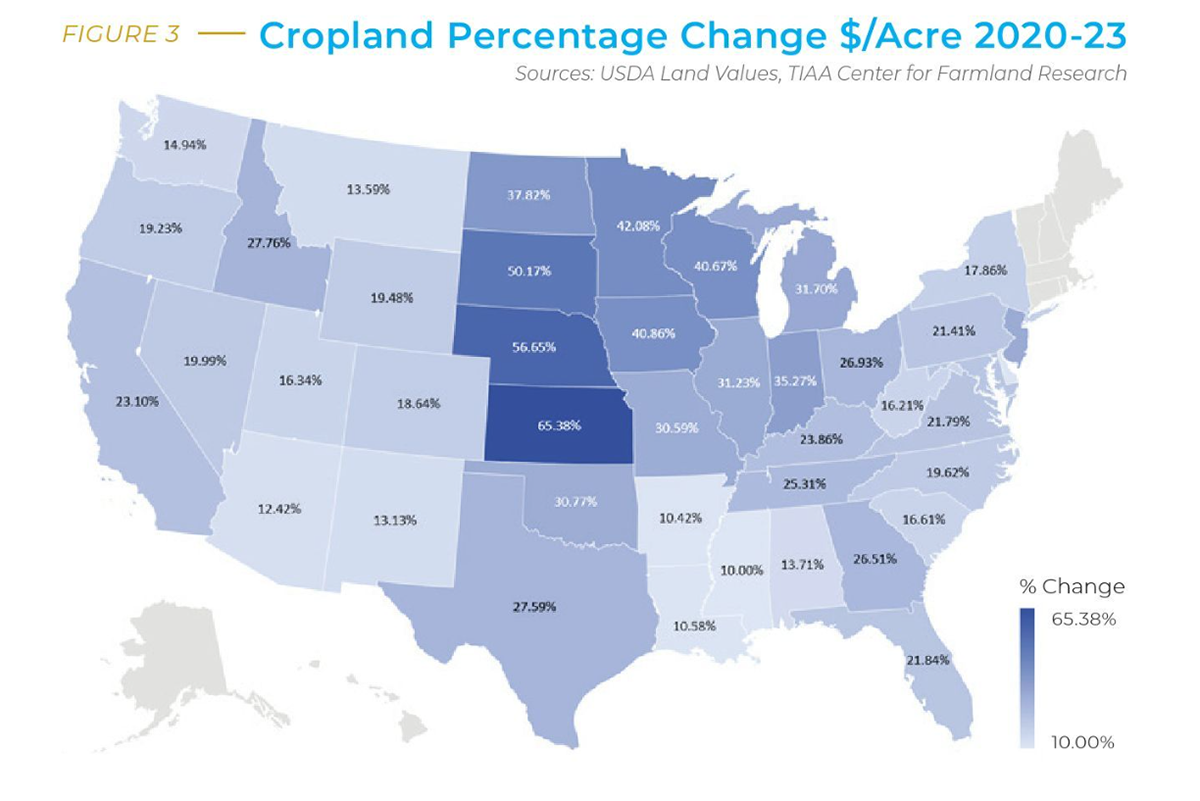

Using a combination of data with boots on the ground experience, Peoples Company has released its fourth annual land values report.

The report shows a three-year period of remarkable land appreciation across the country – something Bruce Sherrick, professor and director of the TIAA Center for Farmland Research at the University of Illinois, says has not been surprising.

“We kind of have a rolling narrative around this and quite often people will remark it’s shocking that farmland almost anticipated inflation or that it’s shocking how well that’s done through time. And I don’t think I’m surprised by that,” he says. “I’m surprised by the accuracy or the degree or the strength of that relationship if anything.”

Annual rates of return have been in the double digits for many regions. In the Northern Plains region specifically, the rate of change in the past year has been especially high.

“In the last year, what we’ve seen is really quite remarkable in the middle of the country,” Sherrick says. “That area has kind of caught up to previous years in the Midwest and Lake states.”

As far as what’s affecting land values in the rest of the country, Peoples Company breaks the data into eight regions.

Cropland values rose by 7.2% in the northern Plains this summer, said agricultural bankers in a quarterly survey by the Minneapolis Federal Reserve Bank. Land values rose even as farm income declined from last summer, lenders said, due to high production costs and lower commodity prices, with a decline expected for this fall, too.

“The outlook for farm capital spending is also contractionary, while lenders expect household spending to flatten,” said the Minneapolis Fed. “More than a third of lenders expect loan demand to increase despite higher interest rates, likely as a result of the tightening cash positions of agricultural producers.”

While the value of unirrigated cropland rose by 7.2%, irrigated cropland surged by 12.8%, according to lenders. Ranch and pastureland values grew by 2.1%. Several bankers noted pressure behind rising land values, such as hunters seeking recreational land and investors purchasing tracts. A Montana banker said higher prices were “making it next to impossible for the next generation to purchase or even lease land to farm or raise livestock.”

During 2022, we witnessed prime farmland selling in excess of $20,000 per acre, and this trend persisted throughout the balance of 2022 and extended into 2023. Though the rate of appreciation was not as dramatic as observed during the period between July 2021 and July 2022, the increase in value remains substantial.

Following is a brief snapshot of those benchmark changes from the 2022 to 2023 update.

Northern/Western Illinois Illinois farmland is classified under a universally accepted soil survey system that breaks land down into quality classifications based on productivity indexes. While values and yields for each cropland type tend to vary by location, the relative productivity does not.

The chart below illustrates changes by cropland type for the northern and western Illinois benchmarks. Values across A, B and C farm types increased an average of +11.2%. One of 19 benchmarks was unchanged, seven were up less than 10%, six were up 10-20%, and five benchmarks were up in excess of 20%.

New economic drivers are emerging that will forever change the landscape of agriculture and the value of farmland.

Location and yield will always be important, but changes in crop and animal genetics, climate shifts and new technologies are escalating in importance. Subtle and decades in the making, these market movers will create opportunities and challenges for both buyers and sellers of farmland.

North Dakota’s Joe Morken has been watching land prices in the Red River Valley increase for more than 25 years. The third generation to farm in the Casselton area, Morken says a shift out of wheat and into corn has been pivotal for his family’s nonirrigated operation.

“You can’t understate the value of genetics when it comes to corn production here,” he says. “Back in the 1980s, if you could break 100 bushels to the acre on corn, that was really doing something. Today’s earlier-maturing genetics allow us to double that some years. Add to that the growth we’ve seen in the ethanol industries in this region, and we have good reason to keep planting corn. It’s changed the focus of our business model.”

Those opportunities haven’t come without challenges. Morken says extreme volatility in fertilizer prices has been especially tough to adapt to as a corn producer. Last year, he booked urea at $1,000 per ton; this year, he’s looking at $400 to $500 per ton. The other challenge is labor. Morken says hiring drivers to keep trucks and grain carts running for combines in a tight harvest window is a major hurdle. But, the area’s increased productivity and cropping options have positively impacted land values in the region, he believes.

“In the Red River Valley, it’s not just corn that pays the bills, it’s soybeans, and it’s sugar beets,” he notes. All of which has drawn more interest to this land market.

This year, the state’s annual report on rental rates showed a wide range for nonirrigated cropland, from as low as $29.20 per acre to up to $150.50 per acre. In Cass County, where Morken farms, average rents were reported at $120 per acre. The USDA’s annual “Land Values” report, released in August, put North Dakota cropland at an average price of $2,660 per acre, marking a 13.2% increase over 2022.

“Land prices have increased substantially,” Morken explains. “In my opinion, strong profits in 2022 are one of the key reasons. Beans, corn … all commodity prices have been up. So, there is more money out there. And, on the eastern side of the Dakotas, we see a strong investor side to the market pushing prices even higher. They come out of the cities, buy land and don’t even farm it.”

:max_bytes(150000):strip_icc():format(webp)/green-energy-indiana-wind-turbine-farm-and-soybean-field-182920989-0c19aacbec864783a77eca8a44545fa7.jpg)

:max_bytes(150000):strip_icc():format(webp)/SUELFLOW.090-2-3b47d6dad05d4c9b9e21f09ca1720417.jpg)